Capital Follows Culture

Why money migrates toward environments it cannot create

There is a persistent belief in business and investing that capital is the primary driver of outcomes. Secure the funding, attract the investment, allocate the resources, and results will follow. This assumption shapes how organizations are built, how decisions are made, and how success is measured.

It is also, in most cases, backwards.

I’ve spent a lot of time studying what makes certain organizations compound value over long periods while others, despite abundant funding, stagnate or destroy it. The pattern I keep coming back to is that capital does not create the conditions for compounding. It responds to them. The environments where money produces durable returns are rarely the ones where money arrived first. They are the ones where something else was already in place: a set of shared operating principles, decision-making norms, and behavioral standards that most organizations call culture but few treat as infrastructure.

The distinction matters because it changes what leaders should prioritize. If capital drives outcomes, the primary tasks are fundraising, budgeting, and allocation. If culture drives outcomes and capital follows, then the primary task is building the environment that makes allocation effective in the first place.

The Evidence Is Hard to Ignore

Consider how talent moves. Top performers can go wherever compensation is highest, wherever resources are most abundant, wherever the balance sheet looks strongest. And yet, consistently, talent migrates toward environments where it can operate at its highest level. The key factor is not compensation alone; it is whether the environment enhances or limits an individual’s capabilities.

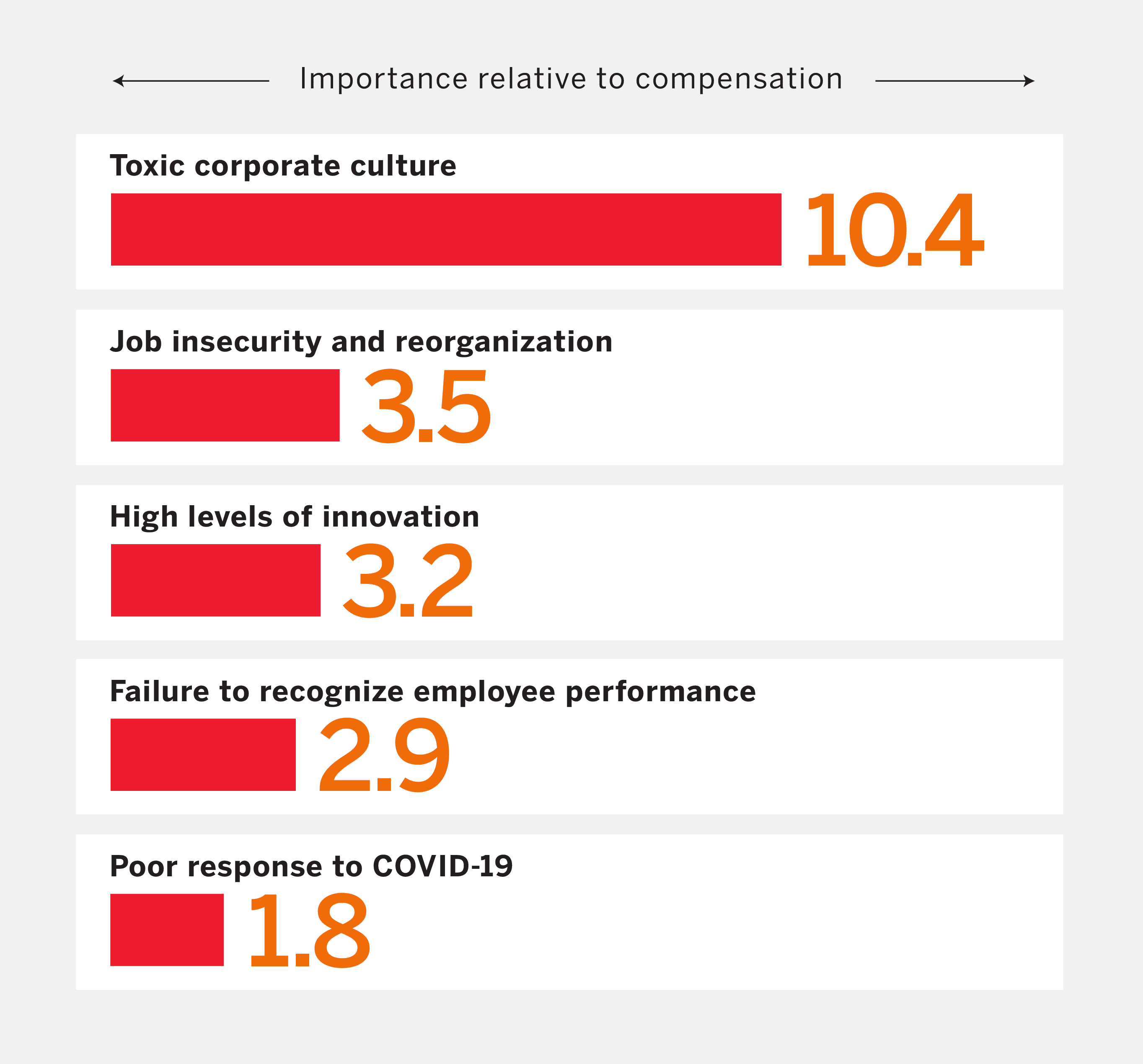

This is not just a soft intuition. MIT Sloan Management Review published research in 2022 analyzing 34 million employee profiles and over 1.4 million Glassdoor reviews and found that toxic corporate culture was 10.4 times more predictive of employee attrition than compensation. Let that sink in. Not twice as predictive, not three times. Over ten times. Compensation ranked 16th among all topics in terms of predicting turnover. In other words, people leave bad cultures far more readily than they leave low salaries.

And the cost of getting this wrong is severe. Gallup estimates that replacing leaders and managers costs around 200% of their annual salary, while replacing technical employees costs roughly 80% and replacing frontline workers about 40%. When a company with a weak culture churns through employees at an above-average rate, the compounding costs of replacement, retraining, and lost institutional knowledge become a structural drag on returns. Organizations without strong internal cultures spend more capital to achieve the same outcomes, often without understanding why their cost structure keeps expanding while results plateau.

The Compounding Mechanism

The mechanism here is simple but profound: culture determines how capital is processed. Two organizations can receive identical funding and deploy it in opposite directions, not because their strategies differ on paper, but because their internal operating environments process information, make decisions, and respond to feedback at fundamentally different speeds and qualities.

I think of it this way. If I give $10 million to an organization with clear decision-making norms, aligned incentives, and strong institutional memory, that capital gets deployed efficiently, iterated on quickly, and compounded over time. If I give the same $10 million to an organization plagued by internal friction, misaligned incentives, and high turnover, a large chunk of that capital goes toward simply maintaining the organization rather than growing it. The input is identical; the output is entirely different.

Warren Buffett articulated this principle clearly in his 2010 shareholder letter, describing how every aspect of Berkshire Hathaway’s operations was designed with the preservation of its culture in mind. His point was not about cultural idealism. It was about capital protection. A culture that attracts aligned operators and repels misaligned ones reduces the single largest source of value destruction in any organization: poor internal decision-making.

The recent transition at Berkshire Hathaway from Buffett to Greg Abel illustrates this perfectly. Abel’s first shareholder letter in February 2026 was essentially an extended pledge to preserve Berkshire’s culture. He described it as Berkshire’s most treasured asset, a framing that echoes what Charlie Munger told shareholders at the 2021 annual meeting:

“Greg will keep the culture. That is the most important thing.”

The entire succession conversation at one of the world’s most valuable companies was framed around cultural continuity. That tells you something about where the real value resides.

What Actually Compounds

What compounds in a strong culture is not just money. It is judgment. Every good decision creates context for the next good decision. Every aligned hire makes the next hire more effective. Every retained lesson reduces the cost of the next problem. This is compounding that does not appear on a balance sheet, but it determines what the balance sheet will look like in five years.

The 2025 Cultureful Workplace Culture Report, analyzing over 8,600 employee responses across more than 44 organizations, found that a shift from neutral to positive culture perception corresponds with a 42-point increase in overall culture health scores, and that visible leadership care is associated with 25% higher retention rates and 30% to 40% lower turnover costs. For a 1,000-person organization, that alone can represent $500,000 to $1 million in annual savings. These are not abstract numbers. They show up in operating margins, in customer retention, and ultimately in the durability of the business.

The reverse is equally true. Cultural erosion compounds gradually and then suddenly. When decision-making quality declines, the first symptom is not financial loss. It is increased friction: longer approval processes, more misaligned initiatives, and higher turnover among the people who notice the shift before anyone else. The Gallup data support this: managers account for 70% of the variance in team engagement, and when manager engagement dropped from 30% to 27% between 2023 and 2024, the downstream effects rippled through entire organizations. Financial deterioration follows, but by the time capital metrics reflect the problem, the underlying cause has been compounding for years.

Implications for Investors and Operators

This is why some organizations can absorb shocks that destroy their competitors. It is also why some well-capitalized companies fail despite having every financial advantage. The difference is not in the resources available, but in the substrate on which those resources operate.

For investors, this provides a practical framework. Financial statements reveal where capital has been. Culture reveals where it is going. I would argue that any serious evaluation of a company’s long-term prospects needs to go beyond the income statement and balance sheet and into the less quantifiable but arguably more predictive territory of decision-making quality, talent retention patterns, and organizational coherence.

For operators, the implication is different but equally concrete. Building culture is not an exercise in values statements or team retreats. It is the creation of an environment in which every unit of capital, time, and attention produces more than it would elsewhere. This is what makes culture an asset class: not because it feels important, but because it determines the return on everything else.

Capital is abundant. It flows globally, seeking returns, reacting to signals, and moving toward opportunity. What remains scarce is the environment that transforms capital into durable value. Money can buy infrastructure, talent, technology, distribution, and time. What it cannot buy is the organizational substrate that makes all of those inputs productive.

Capital follows culture because it has no other rational choice.