Comfort As Risk

What happens when stability lasts long enough to become its own threat

There is a particular phase in the life of a society that rarely gets examined while it is happening: the period when things work, when institutions function, when expectations are met with reasonable consistency.

This phase does not produce headlines. It produces something more consequential: a gradual, invisible restructuring of how we collectively perceive risk.

The longer stability lasts, the more it changes the internal structure of the systems operating inside it. Not because anything breaks, but because everything adapts to the assumption that nothing will.

Minsky Beyond Finance

Hyman Minsky observed that “stability is destabilizing” in the context of financial markets. But the principle operates well beyond finance, and I think it deserves far more attention than it gets applied to institutions, social contracts, and the collective psychology of populations that have lived long enough inside a stable environment to forget that stability is a condition, not a permanent state.

The mechanism is not dramatic. It works through accumulation.

Each year of uninterrupted stability reinforces a set of assumptions: that current conditions are the baseline, that variance will remain within familiar ranges, that the systems supporting daily life will continue to function as they have. These assumptions are not irrational. They are the correct reading of recent evidence. The problem is that they become structural. They get embedded into planning horizons, career choices, debt levels, institutional design, and political expectations.

What is not changing is the external environment. What changes is the threshold of what a society considers normal.

What a Lowered Comfort Threshold Looks Like

This is where the concept of “comfort as risk” becomes useful. It is the point at which a population’s tolerance for disruption has declined so far that even moderate volatility, the kind that previous generations absorbed without crisis, becomes destabilizing.

The threshold is not a fixed line. It moves, and it moves in one direction during prolonged stability: downward.

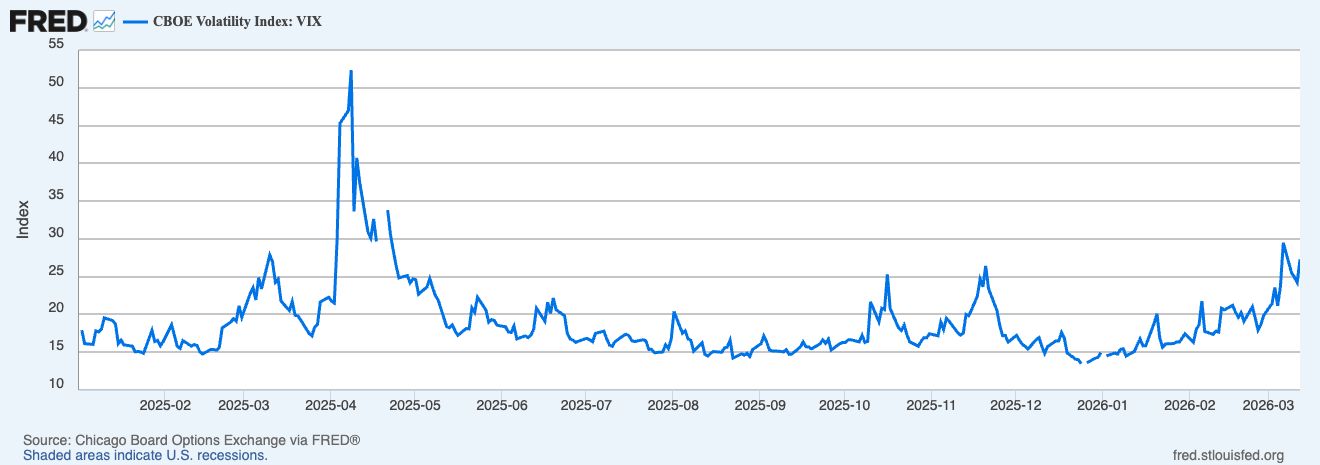

I saw a clean illustration of this dynamic in the VIX over the past year. Throughout most of early 2025, the VIX traded at subdued levels, with implied volatility across major indices well below historical averages. The market was not just calm; it had structurally recalibrated its expectations around calm. The proliferation of zero-days-to-expiration (0DTE) options, which now account for a massive share of daily options volume, further suppressed measured volatility, creating what some analysts described as a “coiled spring” dynamic: the appearance of stability masking a fragile underlying structure.

Then came April 2025. Trump’s “Liberation Day” tariff announcements on April 2nd sent the VIX surging to over 50, its highest reading since the onset of the pandemic in 2020. What made this episode remarkable was not just the magnitude but the cause: this was not a financial crisis, not a pandemic, not a war. It was a trade policy announcement. The VIX peaked within five days and reverted within two weeks, but the violence of the reaction told you everything about how compressed the system’s tolerance for disruption had become.

The market recovered, volatility settled back down through the second half of 2025, and then the pattern seems to be repeating in March 2026, when US-Israeli military strikes on Iran. The system had re-compressed its expectations, and once again a geopolitical shock produced a reaction disproportionate to what previous generations of markets would have absorbed without flinching.

That is Minsky operating in real-time, outside the credit cycle.

The Generational Dimension

Consider what happens in a society that has experienced three decades of relative continuity. The generation that built the stability understood its fragility, because they remembered what came before. But the generation that inherited it does not carry that memory. They carry expectations calibrated to the conditions they have always known. Their risk tolerance is not reduced by weakness; it is reduced because they lack an experiential frame of reference for major disruptions.

I think this dynamic is underappreciated. It does not show up in any single data point. It shows up in the aggregate behavior of a population that has systematically reduced its buffers during a period when everything appeared to be going well.

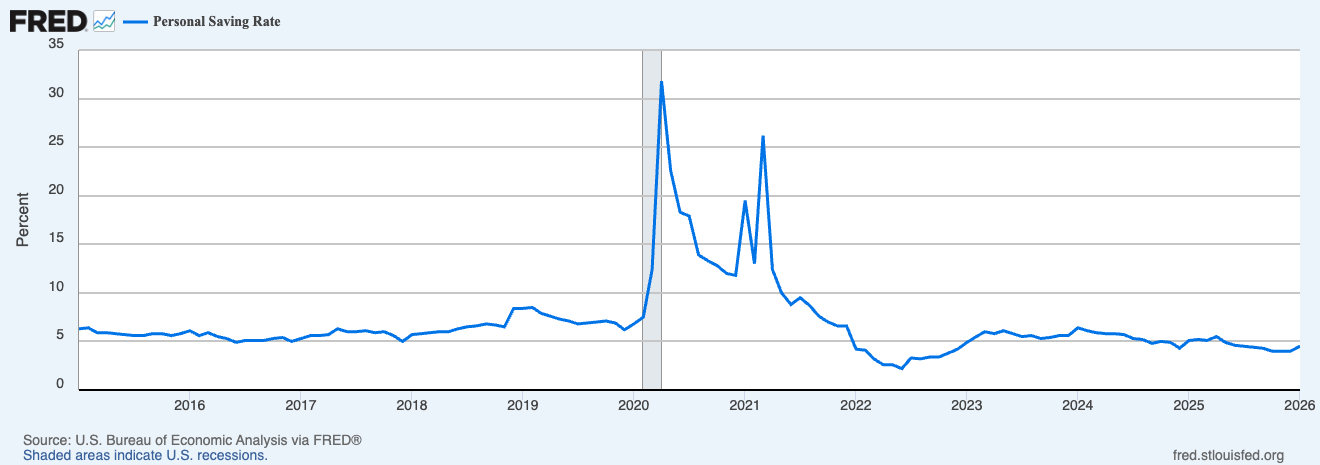

The US personal savings rate hit 3.6% in December 2025, inching toward 2022’s decade-low of roughly 2%. For context, the long-run average is closer to 8-9%. Total household debt reached a record $18.8 trillion as of the fourth quarter of 2025, with credit card balances alone at $1.3 trillion, according to the New York Fed’s Household Debt and Credit Report. These are not signs of a system in crisis. They are signs of a population that has internalized the assumption that current conditions will persist, that income will keep flowing, that disruptions will remain small and temporary. In other words, a population that has adapted its financial behavior to stability, exactly as Minsky’s framework would predict.

The recalibration is invisible precisely because it happens inside the framework of normalcy. No one announces that the comfort threshold has changed. No institution publishes a report stating that collective resilience has declined. The indicators that would signal this shift largely do not exist in standard measurement, because the measurement systems were designed during the stable period and reflect its assumptions.

What It Looks Like From the Inside

What does a society with a lowered comfort threshold look like from the inside?

It looks functional. It looks prosperous. It looks like the system is working.

And in many ways it is. But the distance between current operating conditions and the point at which the system would face genuine stress has narrowed. The margin of safety has compressed, not because the threats have grown, but because the capacity to absorb them has diminished.

This applies beyond household balance sheets. It applies to the physical infrastructure that a society relies on. The American Society of Civil Engineers gave US infrastructure an overall grade of C in its 2025 Report Card, the highest grade since the assessment began in 1998, but still classified as “mediocre, requires attention.” Nine of the eighteen categories evaluated, including energy, transit, and dams, received grades in the D range. The energy grid was actually downgraded from C- to D+, with the ASCE warning that electricity infrastructure capacity may not keep pace with future demand. The estimated funding gap to bring systems to an adequate condition is $3.7 trillion over the next decade.

This is what Minsky looks like in physical form. The infrastructure works. It works today. It will probably work tomorrow. But the margin between “working” and “failing” has been gradually eroding for decades, during exactly the period when the absence of failure convinced everyone that the systems were fine.

The Question That Matters

Where does this leave the question of cycles?

Cycles are often discussed as though they are driven by external events: a financial crash, a geopolitical shift, a technological disruption. But the research on societal and financial cycles suggests something more uncomfortable. The conditions for the next phase of instability are frequently generated during the preceding phase of stability. The accumulation of hidden fragility, the erosion of adaptive capacity, and the narrowing of what a society can tolerate without fracturing are not caused by the crisis. They are caused by the comfort that precedes it.

The relevant question, then, is not the one most people ask.

It is not: when will the next disruption arrive? What form will instability take? How do we predict the turning point?

The relevant question is: what has this period of stability done to our capacity to navigate what comes after it?

That question is harder to answer because it requires examining the present not as a state of achievement but as a process of slow transformation. It requires acknowledging that the conditions we interpret as strength may, quietly and without visible symptoms, be producing the preconditions for fragility.

I think we are further along in this process than most people realize. Household debt at record levels, savings rates near historical lows, infrastructure running on thinning margins, and a financial system that spent the better part of 2025 pricing in uninterrupted tranquility before being jolted twice by events that, in historical terms, were not extraordinary. None of these facts, taken individually, signals a crisis. Taken together, they describe a system that has progressively narrowed its buffer against disruption.

Societies do not become vulnerable the moment the crisis arrives. They become vulnerable long before, during the years when everything appears to be working. The comfort threshold shifts in silence, and by the time it becomes measurable, the distance it has traveled is already significant.

The biggest risk is not the event that disrupts stability. It is the stability itself, and what it gradually makes of those who live inside it.