Toward a Programmable Economy

How ownership that carries its own logic reshapes markets, companies, and capital flows

There’s a lot of discussion right now about tokenization and the transformation of financial infrastructure. Most of it focuses on blockchain adoption, which institutions are involved, and where regulation is headed. Those are fine topics, but I think they miss the more interesting question: what changes structurally when assets become programmable?

The Cost You Don’t See in the Current System

The financial system we have today operates on a fundamental separation: an asset exists in one place, the record of who owns it exists in another, and the process of transferring it requires a chain of intermediaries. Brokers, clearinghouses, custodians, transfer agents, settlement systems. Each layer adds time, cost, and counterparty risk.

This architecture wasn’t designed to be inefficient. It was designed for a world where trust required institutional verification at every step. When records were physical, intermediaries were the only mechanism capable of guaranteeing that ownership was legitimate and transfers were valid. That made sense.

Digitization made the system faster. Electronic records replaced paper. Settlement times compressed significantly over the decades, from five business days before 1993, to three days in 1993, then to two days in 2017, and finally to one business day when the SEC moved to T+1 in May 2024. Communication became instantaneous.

But the underlying architecture remained intact. The intermediaries became digital, not unnecessary. Reconciliation between separate databases still happens daily. Capital still locks up in transit between trade execution and settlement. The DTCC has noted that even after the shift to T+2, over $5 billion was still held in risk margin on average to manage counterparty default risk in the system. The cost of maintaining this infrastructure is embedded in every transaction, invisible but real.

The system works. It has worked for decades. I'm not arguing it's broken. But I do think the gap between what the system costs to maintain and what it actually needs to cost is wider than most people realize, and that gap is where the real opportunity sits.

What a Programmable Asset Actually Does

I want to be precise here because there’s a lot of loose language around this topic. A programmable asset is not simply a digital version of a traditional asset. It is an asset that carries its own operational logic.

Take a tokenized bond. It doesn’t just exist as a record on a blockchain. It can calculate its own interest payments, automatically distribute them to current holders, enforce transfer restrictions in accordance with regulatory requirements, and settle in seconds rather than days. The bond itself becomes the infrastructure.

This distinction matters because it eliminates the separation that defines the current system. In the traditional model, an asset relies on external records, external management, and external enforcement. In the programmable model, all three are embedded in the asset itself.

When the logic moves inside the asset, several things happen at once. Settlement compresses from days to seconds. Reconciliation between separate ledgers becomes unnecessary. Fractional ownership becomes operationally simple rather than complex and expensive to manage. And assets that were previously uneconomical to issue, manage, or trade suddenly become viable.

The world’s largest financial institutions are actively building on this logic, and I think that’s worth paying attention to. BlackRock launched its tokenized money market fund, BUIDL, on Ethereum in 2024, and by late 2025, it had grown past $2.5 billion in assets. JPMorgan launched its own tokenized money market fund, MONY, on Ethereum in December 2025, seeded with $100 million. JPMorgan’s Kinexys platform has processed over $1.5 trillion in tokenized transactions. Goldman Sachs and BNY Mellon have partnered to offer tokenized money market fund shares to institutional clients. Franklin Templeton launched the first mutual fund on a blockchain in 2021 and has continued to expand since.

These firms are not doing this because of ideological alignment with decentralization. They’re doing it because the operational advantages compound at scale in ways that digitization alone never achieved. As JPMorgan’s John Donohue put it, there is massive client interest in tokenization, and the bank expects other globally systemically important banks to follow.

The Cascade Beyond Capital Markets

The financial system is the most obvious application, but I think the logic extends further than most people realize. It applies to any domain where ownership, provenance, or entitlement matters.

Consider companies that produce physical goods. Under the current model, the moment a product is sold, the relationship between producer and product effectively ends. The company has no visibility into subsequent transfers, captures no value from secondary transactions, and lacks a mechanism to maintain an ongoing relationship with whoever holds the product at any given time.

When ownership becomes programmable, the product itself can carry an evolving record of its entire history. But more importantly, the producer can embed conditions that persist through every subsequent transfer: a percentage of every resale returns to the original creator, access to services or experiences is tied to verified ownership, authenticity verification happens at the protocol level, and the customer relationship becomes portable across platforms and markets.

This changes the economics of producing something. The value of a product is no longer captured entirely at the point of first sale. It extends across the entire lifecycle. My view is that companies that understand this early will build differently, though I’d also note that we’re still in the very early stages of figuring out what this looks like in practice outside of digital collectibles.

The Macro Picture

If you zoom out far enough, the pattern becomes clear. In the current economy, the distance between assets and the systems required to manage them is filled with intermediaries, processes, and institutions that extract value at every step. I want to be clear that this is not because these intermediaries are parasitic. It’s because the old architecture required them. Without third-party verification, the system could not function.

A programmable economy reduces the need for that verification by embedding it in the assets themselves. The implications scale across every sector where ownership matters.

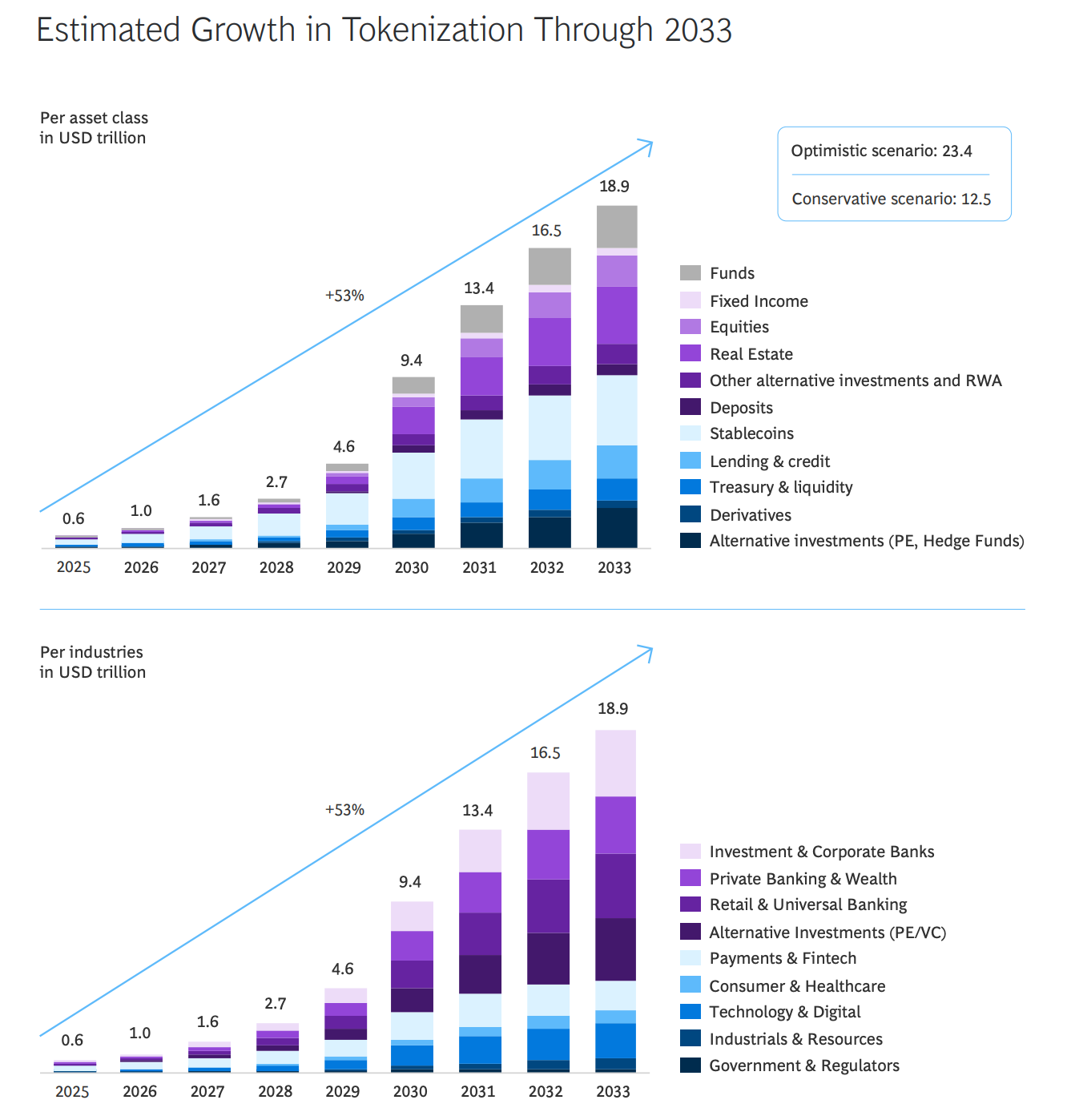

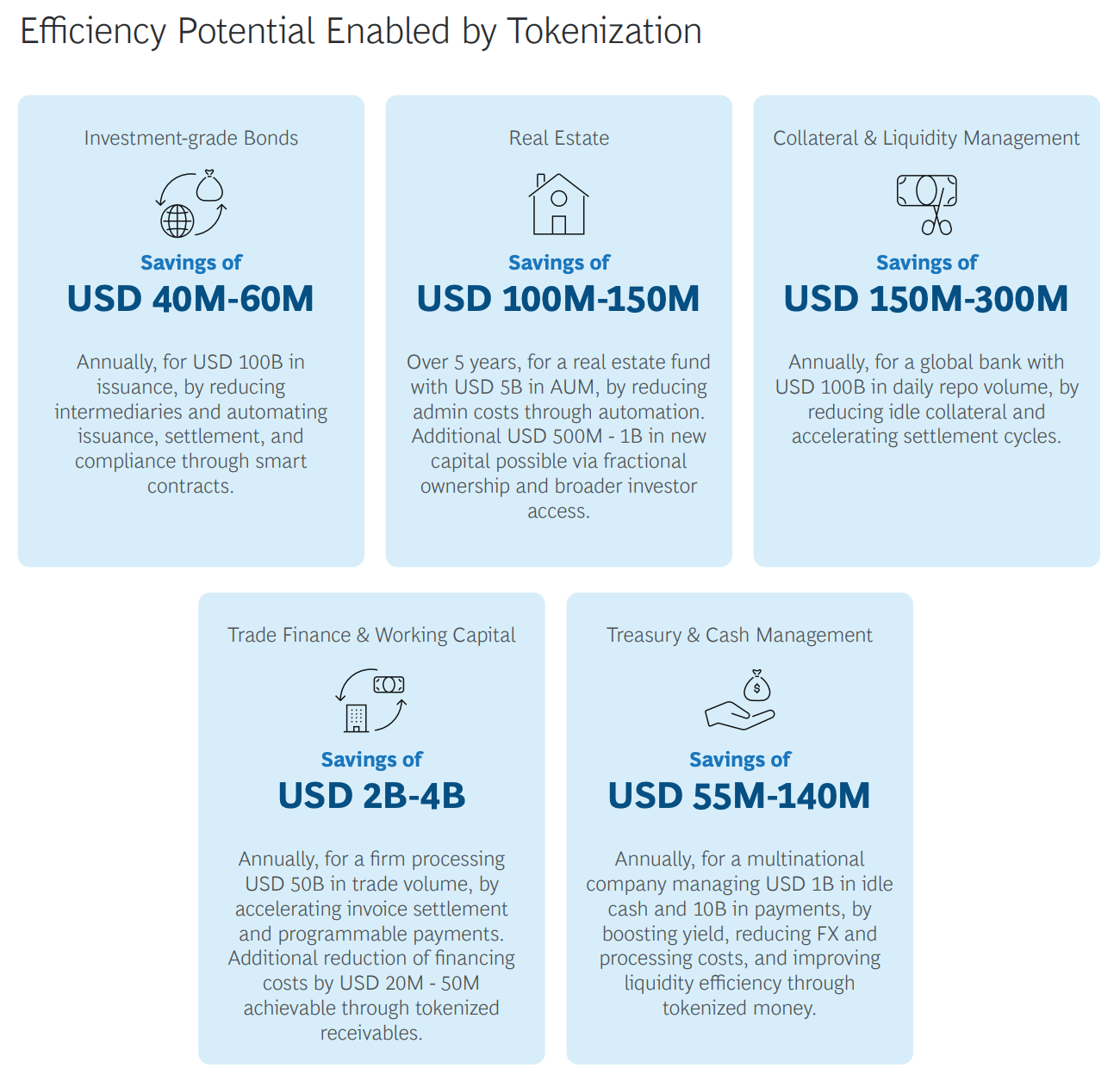

In capital markets, settlement infrastructure compresses, capital efficiency increases, and the universe of issuable assets expands. The BCG-Ripple report estimates that tokenized collateral management alone could save $150 to $300 million for every $100 billion in daily repo transactions. In physical goods, producer-to-consumer relationships extend beyond the first sale, secondary markets become visible and participatory, and the economics of the product lifecycle change. In real estate, fractional ownership becomes operationally simple, cross-border investment friction decreases, and the distribution of rental income automates. Real estate tokenization was already valued at roughly $20 billion in 2025. In intellectual property, royalties can flow automatically across every use and transfer, without manual tracking or institutional intermediation.

The common thread across all of this is not blockchain as a technology. It’s the collapse of the operational overhead that currently sits between an asset and its owner.

Now, I should also be honest about the uncertainties. The BCG-Ripple report itself revised its 2022 projections downward, from $16 trillion by 2030 to $9.4 trillion by 2030. That’s a significant reduction, and it reflects real obstacles: fragmented infrastructure, limited interoperability across platforms, uneven regulatory progress across jurisdictions, and inconsistent custody frameworks. These are not trivial problems.

My base expectation is that the programmable asset model does eventually reshape large parts of the financial system and beyond, but the timeline is genuinely uncertain. The institutions are moving. The technology works at smaller scales. The regulatory environment is slowly clarifying, with the EU’s MiCA framework, Singapore’s Project Guardian, and in the US, the passage of the GENIUS Act in 2025. Whether the market reaches $18.9 trillion by 2033 or something more modest, the direction seems fairly clear to me. The economy that forms around programmable assets will operate on a different logic than the one we have now. The question is not if, but how quickly, and where the most friction remains.