Who Owns Decentralization

BlackRock, JPMorgan, and Fidelity are building on blockchain faster than any protocol community

Blockchain entered public consciousness as a direct challenge to traditional financial institutions. The core thesis was built on a few clear principles: eliminate intermediaries, distribute control, and let code replace trust.

Fifteen years later, the technology has evolved significantly. But the intermediaries haven’t disappeared. They’ve adopted it.

I think the most consequential blockchain development of 2025 was not a new protocol, a consensus mechanism, or a decentralized application. It was the world’s largest asset manager quietly becoming one of the most significant builders on Ethereum. BlackRock’s tokenized money market fund, BUIDL, peaked at roughly $2.9 billion in total value by mid-2025, according to RWA.xyz data, making it the largest tokenized fund on public blockchains. Even after experiencing some outflows in the second half of the year, with assets settling around $2.2 billion, it remains the clearest signal of where blockchain development is actually heading.

What Was Promised

The original thesis was simple and radical. Financial systems depend on intermediaries: banks, clearinghouses, custodians, and brokers. Each one adds cost, delay, and a layer of control that users cannot bypass. Blockchain could replace all of them with transparent, programmable, self-executing code.

The vision attracted capital, talent, and ideological commitment. Decentralized protocols would process transactions without banks. Smart contracts would enforce agreements without lawyers. Tokenized assets would trade without brokers. The entire apparatus of financial intermediation would be rendered unnecessary by better architecture.

The promise was that institutional control, fees, barriers to access, and gatekeeping would shrink, while individual sovereignty, transparency, and permissionless participation would grow.

For several years, the trajectory seemed to confirm the thesis. DeFi protocols demonstrated that lending, borrowing, and trading could operate without traditional intermediaries. Total value locked grew from nearly zero to tens of billions. The technology functioned effectively. But disintermediation didn’t happen.

Who Actually Built It

The transition happened gradually and then all at once. Traditional financial institutions started to view blockchain not as a competitor but as infrastructure. They found a technology that could address longstanding problems they actually cared about: settlement speed, cross-border inefficiencies, collateral management, and round-the-clock market access.

JPMorgan’s Kinexys platform has exceeded $1.5 trillion in notional value since its inception and processes over $2 billion in daily transaction volume. Its Intraday Repo application alone has enabled $300 billion in trading volume, with cross-chain settlement tests involving tokenized U.S. Treasuries against dollar deposits now underway with partners like Ondo Finance and Chainlink. Franklin Templeton moved its U.S. Government Money Market Fund onto the public blockchain. Fidelity launched the Fidelity Digital Interest Token on Ethereum in August 2025, a blockchain-based share class of its Treasury money market fund that surpassed $200 million in assets shortly after launch. Nasdaq filed with the SEC on September 8, 2025, to allow tokenized equity securities and exchange-traded products to trade alongside traditional stocks on its exchange. And on July 18, 2025, President Trump signed the GENIUS Act into law, creating the first federal regulatory framework for payment stablecoins and effectively building the legal foundation for institutional-scale adoption.

So the question becomes: who contributed what?

Decentralized communities built the protocols. They contributed technological originality, speed of iteration, and ideological conviction. Institutions brought capital, regulatory relationships, compliance infrastructure, and distribution networks capable of reaching sovereign-scale capital. The communities created the innovation. The institutions created the market.

The outcome was unexpected by both sides. Larry Fink wrote in his 2025 annual letter to investors that every stock, every bond, and every fund can be tokenized, and that doing so will revolutionize investing.

The total market for tokenized real-world assets surpassed $33 billion by late 2025, according to RWA.xyz and multiple market trackers. By November, some estimates placed it above $35 billion. Projections from various analysts, including those at McKinsey, Galaxy Digital, and Standard Chartered, range from roughly $2 trillion to $10 trillion by 2030, depending on assumptions about regulatory progress and institutional adoption. But the entities driving this growth are not DAOs or decentralized collectives. They are the firms that manage pension funds, sovereign wealth, and global capital flows.

The Product Survived. The Ideology Did Not.

I think this situation deserves an honest assessment without ideological attachment to either side.

The technology has delivered on much of its initial promise. Settlement is faster. Transparency is higher. Access is broader. Fractional ownership works. Markets can function continuously, across borders, without the settlement delays and intermediary layers that defined traditional finance for decades.

But the distribution of power has not shifted in the direction the founders intended. If anything, it has become more concentrated.

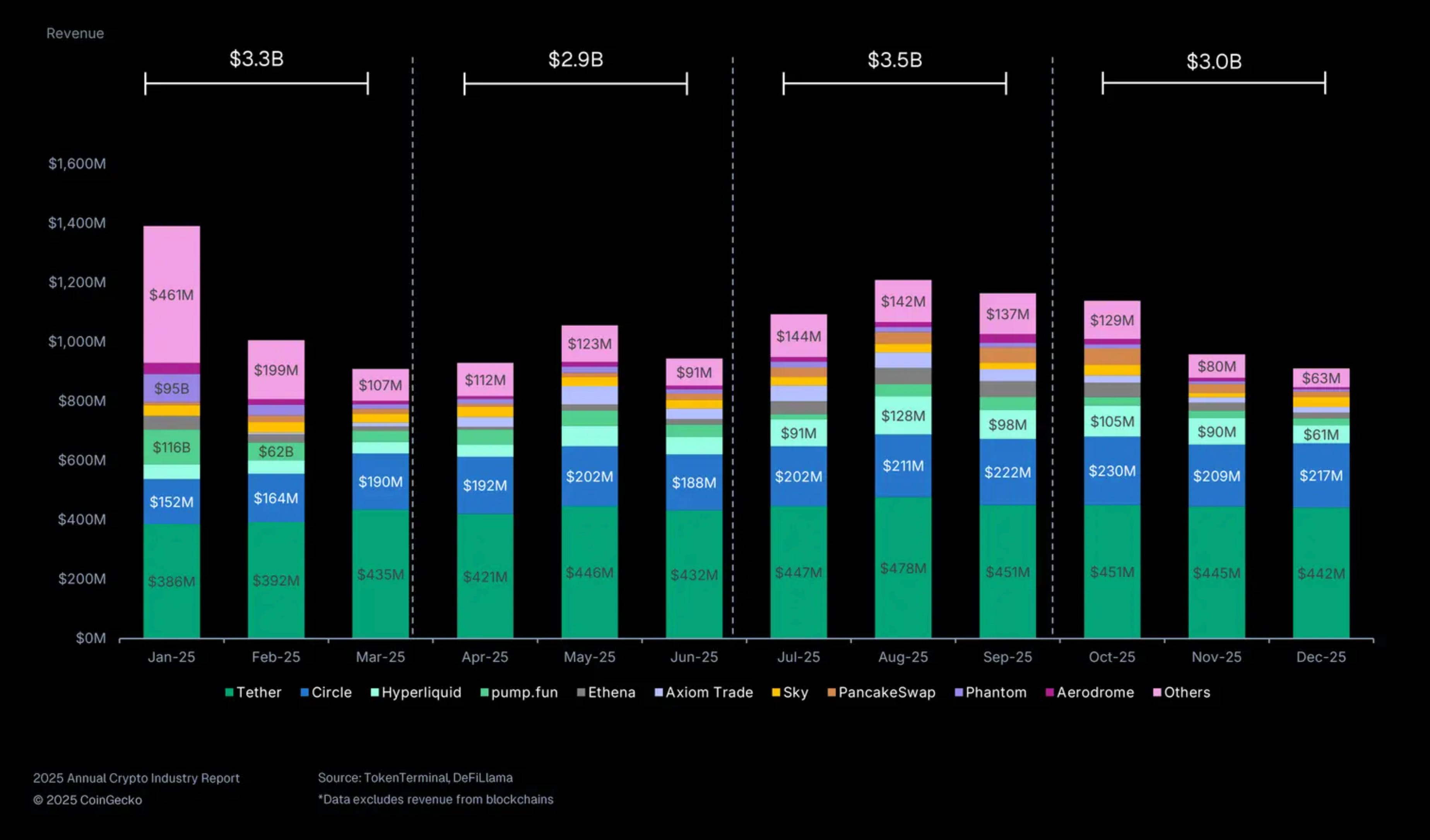

The revenue structure tells the story pretty clearly. In DeFi, Tether alone captured around 54% of all revenue in 2025, according to DL News’s State of DeFi analysis. The broader CoinGecko annual report, which tracked 168 revenue-generating protocols, put Tether’s share at 41.9% of total crypto protocol revenue, or roughly $5.2 billion. Either way you measure it, that’s an extraordinary level of concentration for an ecosystem built on the premise of distribution. In tokenized assets, a handful of traditional asset managers control the majority of the market. BlackRock, Securitize, Franklin Templeton, and Ondo Finance account for the lion’s share of issuance volume.

The pattern is consistent with every previous technology cycle I can think of. Open systems are built by decentralized communities and captured by entities with the resources, relationships, and regulatory standing to operate at scale. It happened with the internet. It happened with the mobile. And it’s happening with blockchain.

My view is that this is neither surprising nor necessarily bad, though I understand why it frustrates people who believed in the original vision. Decentralization sets up the framework. Centralization runs the operations. Blockchain is changing finance. But it is not changing who runs it.

That’s not a prediction. It’s an observation about where we are right now. And I think the sooner participants on both sides of this divide accept it, the more productive the conversation about what comes next will be.